The Great Solana Reallocation: Who Really Wins from SIMD-228?

Daniel Asaboro

Daniel Asaboro

The greatest trick VCs ever pulled was convincing retail investors that high staking yields were in their interest.

For years, Solana's inflation-driven staking rewards—currently around 4.7% annually—have been positioned as a feature, not a bug. "Stake your SOL and earn passive income!" the narrative goes. Meanwhile, almost two-thirds of Solana's supply sits idle in validator stake accounts, unavailable for DeFi, NFTs, or any of the activities that actually drive network value.

Make no mistake though as this arrangement serves some groups quite well.

Large validators earn steady commissions. Institutions with massive token allocations receive predictable yield while waiting for unlock dates. And retail investors? They watch as their staking "gains" are offset by the very inflation creating those rewards—a monetary treadmill disguised as forward progress.

SIMD-228, the Solana Improvement Document set for voting on March 7th, proposes to fundamentally reshape this dynamic. By tying inflation rates directly to staking participation, it creates something unprecedented in Layer 1 cryptoeconomics: a self-balancing monetary policy that adapts to network conditions.

To put it simply, when too much SOL is staked (above 50%), inflation plummets. When too little is staked (below 33%), inflation increases.

The proposal represents more than a technical adjustment—it's a deliberate reallocation of economic incentives that will create clear winners and losers across the Solana ecosystem. Smaller validators may struggle to remain profitable. Retail stakers will see yields decrease. But capital will flow from staking into DeFi, NFTs, and other productive uses—potentially transforming Solana from a network where tokens are primarily hoarded to one where they actively circulate.

In this analysis, I'll examine who stands to gain and lose from SIMD-228, the technical mechanics of how it works, and what it reveals about Solana's vision for the future. Whether you're a validator, developer, investor, or user, these changes will reshape your relationship with the network—and understanding them now gives you time to adapt before they take effect.

The Inflationary Mirage: How the Current Model Works

To understand why SIMD-228 represents such a pivotal shift, we need to first unpack Solana's current inflation model and the incentive structures it creates.

Currently, Solana follows a deterministic inflation schedule: it began at 8%, decreases by 15% annually, and will eventually reach a floor of 1.5%. As of early 2025, the inflation rate stands at approximately 4.7%. This means the network is minting roughly 28 million new SOL tokens annually—worth about $4.7 billion at current prices.

These newly minted tokens are distributed to validators and delegators in proportion to their stake. With about 65% of the circulating supply currently staked, the average staking yield sits at around 7.2% APY before fees. After accounting for validator commissions (which range from 0% to 10%), a retail staker might expect a nominal yield between 6.5% and 7%.

Here's where the mirage begins to shimmer: that 7% return is denominated in a currency that's inflating at 4.7% per year. The real purchasing power gain is closer to 2.3%—and that's before considering tax implications.

But the reality is even worse than these numbers suggest. Max Resnick, an economist at Anza, perfectly captured this dynamic with what he calls the "leaky bucket" theory.

a) The Leaky Bucket Theory

The newly minted SOL from inflation doesn't just appear in Stakers' wallets—it passes through a series of extractive mechanisms:

Tax authorities claim their share—up to 37% in the US, where staking rewards are often classified as ordinary income rather than capital gains

Centralized exchanges like Binance and Coinbase take approximately 8% of staking rewards in fees

Validators extract their commission (though many have moved to 0% to remain competitive)

By the time this process is completed, what started as 4.7% inflation might deliver as little as 1.5-2% in real value to the average retail staker. And that's assuming the market doesn't react negatively to the ongoing increase in token supply.

b) The Validator Economics Problem

The current model creates particularly perverse incentives for validators.

If you think about it, in an ideal proof-of-stake system, validators should compete on performance and cost-efficiency. Instead, many Solana validators compete primarily on commission rates, driving them toward unsustainably low levels. According to data in the documents, approximately 49% of validators have set their commission rates to zero, effectively giving up inflation-based revenue entirely.

So how do they survive? Increasingly, validators rely on MEV (Maximal Extractable Value) and priority fees to sustain operations. This creates a system where validators with the most stake have privileged access to the most profitable transaction ordering opportunities—a rich-get-richer dynamic that further concentrates stake.

While the validator economics problem is concerning, it's only one symptom of a more fundamental flaw in the current model which we can boil down to the inefficient allocation of capital. What is it?

c) The Capital Allocation Problem

With 65% of SOL locked in staking, relatively little is available for actually using the network. This creates a curious paradox: Solana has achieved impressive growth in activity and value despite having the majority of its native assets effectively removed from circulation.

As Marius, co-founder of Kamino, noted: "Staking encourages hoarding and reduces financial activity... In a way, it's similar to the Fed raising rates and tightening financial conditions." This artificial restriction on capital flow has created a bottleneck for DeFi growth—Solana DeFi's TVL remains a fraction of Ethereum's, despite Solana's technical advantages in terms of speed and cost.

These fundamental problems—the inflationary mirage, perverse validator incentives, and inefficient capital allocation—set the stage for SIMD-228's radical redesign of Solana's monetary policy. Lets examine how in the next section.

SIMD-228: The Mechanics of a Market-Based Inflation Model

The core mechanism is surprisingly elegant: rather than following a fixed schedule, the inflation rate will adjust based on the percentage of SOL that's staked. The formula looks like this:

i(s) = r * (1 - √s + c * max(1 - √(2s), 0))

Where:

iis the new inflation rateris the current static inflation rate (starting at 4.7%)sis the staking rate (fraction of total supply staked)cis a constant (~3.146, approximately π)

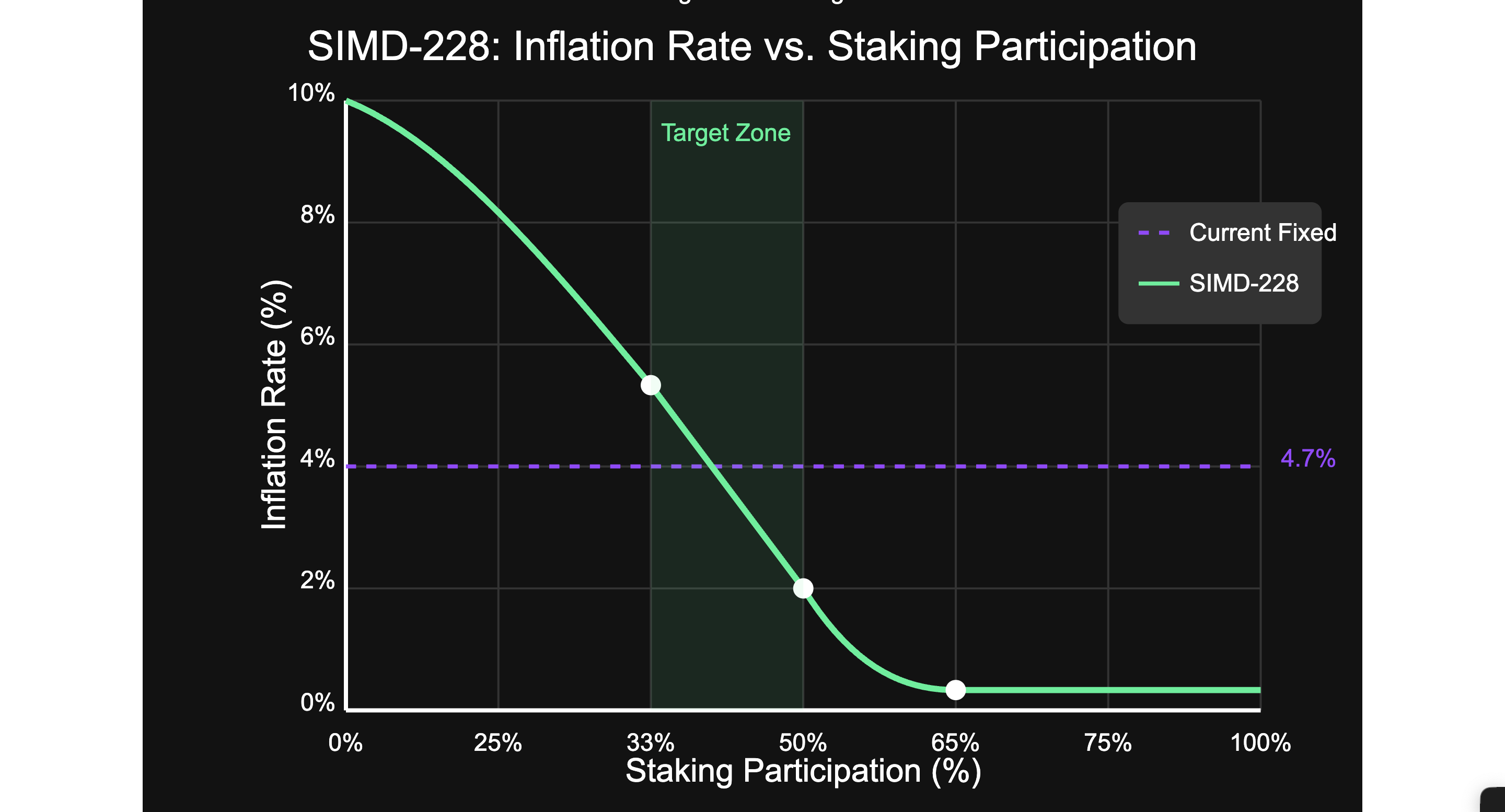

I understand that this might look intimidating, so lets look at the graphical representation

but the practical effects are straightforward:

When staking participation is above 50%, inflation decreases sharply. At the current ~65% staking rate, inflation would drop to approximately 1.4% almost immediately.

When staking participation falls between 33-50%, inflation remains moderate, creating an economic balance that aims to stabilize staking around this range.

When staking participation drops below 33%, inflation increases substantially, even exceeding the current rate, to incentivize more staking and ensure network security.

The implementation plan calls for a 50-epoch transition period (increased from the initially proposed 10 epochs). During this period, the network will gradually interpolate between the old and new inflation rates, giving stakeholders time to adapt.

Why these specific thresholds? From a security perspective, 33% represents a critical threshold. As long as honest validators control more than two-thirds of staked SOL, the network remains secure against certain attack vectors. Above 66% staking, there's little additional security benefit. The 50% target creates a buffer zone that maintains security while freeing up capital for other uses.

With such a fundamental change to Solana's economic structure, it's essential to understand who benefits and who bears the costs of this transition.

Who Wins, Who Loses: A Stakeholder Analysis

Every monetary policy change creates winners and losers. SIMD-228 is no exception. Its impact varies dramatically depending on your role in the Solana ecosystem. From retail holders to large institutional players, the proposal creates a complex web of incentives that will reshape how value flows through the network. So let's examine each major stakeholder group to understand how they'll be affected.

My analysis focuses on 4 groups:

Retail Investors

Venture Capital and Institutional Investors

Validators

Defi Protocols

Let’s look at each in detail:

1) Retail Investors: Short-Term Pain, Long-Term Gain?

For the average retail holder staking their SOL, SIMD-228 looks superficially negative. Staking APYs will likely drop from ~7% to as low as 2-3% if staking participation remains high initially. This represents a significant reduction in passive income, potentially forcing difficult decisions about whether to continue staking.

However, looking deeper, there are several potential compensating factors:

Reduced inflation means less dilution of token value. While yields decrease, so does the rate at which new tokens enter circulation, potentially supporting price appreciation.

Greater capital efficiency as more SOL flows into DeFi and other productive uses, potentially driving overall ecosystem growth and token value.

Improved tax efficiency as lower yields generate fewer taxable events, reducing the "leaky bucket" effect described earlier.

DeFi opportunities may become relatively more attractive, allowing retail users to potentially earn higher risk-adjusted returns than from staking.

The transition will require retail investors to become more active in managing their SOL holdings—no longer can they "set and forget" with staking. This increased complexity represents a real cost, particularly for less sophisticated users.

2) Validators: A Bifurcated Future

For validators, SIMD-228 creates a stark divide between the haves and have-nots.

2a) The Winners: Established, Well-Capitalized Validators

Large validators with significant stakes, established MEV extraction capabilities, and optimized infrastructure will likely weather this transition well. They have diversified revenue streams beyond inflation rewards and economies of scale to operate efficiently even with lower returns.

According to economic modelling in the proposal documents, validators with more than 0.5% of stake typically derive less than 20% of their revenue from inflation commissions, relying more heavily on MEV and priority fees. For these operators, SIMD-228 may even be positive, as it could drive more network activity and transaction volume.

2b) The Losers: Small, Independent Validators

The outlook is considerably bleaker for smaller validators, particularly those with less than 0.05% of stake. Many of these validators are already operating at minimal profitability, with voting costs (~2 SOL per day) consuming a significant portion of their revenue.

The proposal's economic modelling suggests that 3-3.4% of validators (approximately 24-40 validators) would become unprofitable under SIMD-228. Industry sources cited in the documents suggest the real number could be closer to 100 validators—roughly 7-8% of the existing set.

This reduction in the validator set represents a direct trade-off between decentralization and capital efficiency. Solana explicitly chooses to optimize for the latter, betting that a more concentrated but highly performant validator set is better for the network's long-term success than maximizing validator count at the expense of capital efficiency.

It's worth noting that Anza is reportedly working on a vote cost reduction SIMD that could alleviate some pressure on smaller validators. However, the timing of this relief remains uncertain.

3) VCs and Institutional Investors: The Invisible Winners

Perhaps the clearest beneficiaries of SIMD-228 are large institutional token holders—particularly venture capital firms with significant SOL allocations subject to vesting schedules.

Looking at the unlock schedule in the proposal documents, several large unlocks are coming over the next 12-24 months. For example:

March 24, 2025: 600,632 SOL

April 4, 2025: 1,822,843 SOL

April 7, 2025: 702,101 SOL

Under the current model, these tokens are being diluted at 4.7% annually while waiting to unlock. Under SIMD-228, that dilution rate could drop by more than two-thirds, preserving substantially more value for large holders.

Beyond reduced dilution, institutional investors also benefit from increased capital efficiency. Many VC firms have investments across the Solana ecosystem, including DeFi protocols that would benefit from increased liquidity flowing from unstaked SOL.

The proposal's timing—coinciding with a period of significant token unlocks—raises questions about whether these institutional interests played a role in shaping the SIMD-228 timeline. While impossible to prove, the alignment of incentives is noteworthy.

4) DeFi Protocols: A Capital Influx

If SIMD-228 accomplishes its goal of reducing staking participation from 65% to closer to 50%, it would free up approximately 80-90 million SOL (worth over $12 billion at current prices) for other uses.

Where will this capital go? Much of it will likely flow into Solana's DeFi ecosystem, which has been capital-constrained relative to its activity level. This influx could dramatically expand liquidity pools, lending markets, and trading venues.

Specific beneficiaries might include:

Lending platforms like Solend and Kamino, which currently have only about 0.2% of SOL supply in their protocols (compared to Ethereum's Aave, which has around 2% of ETH supply)

DEXs like Raydium, Orca, and Meteora, which would see deeper liquidity and reduced slippage

Liquid staking tokens like Jito, Marinade, and Lido, which offer a middle ground between staking and DeFi participation

The documents highlight that Solana currently has 33% of its TVL in DEXs (compared to Ethereum's 8%), but only 13% in lending (compared to Ethereum's 24%). This suggests particular growth potential in the lending sector.

Technical Implications: Performance vs. Decentralization

Beyond the economic impacts, SIMD-228 has significant technical implications for Solana's performance and security model.

Network Performance Considerations

Solana's technical architecture demands high-performance validators running on enterprise-grade hardware. As the proposal documents note, validators require "beefy machines" costing $900-1,500 per month, plus bandwidth costs and redundant systems. This creates a natural tension between maximizing validator count and ensuring network performance.

By shifting rewards toward transaction processing (MEV and priority fees) rather than passive staking, SIMD-228 aligns validator incentives more closely with network performance. Validators who process transactions most efficiently will capture the most value, creating stronger economic pressure to maintain high-quality infrastructure.

The documents specifically mention that "low-stake validators often cut costs on machines, operating on non-performing infrastructures." To the extent that SIMD-228 weeds out such operators, it could actually improve overall network performance and reliability.

Security Model Evolution

Solana's security has historically relied on a high staking ratio—currently around 65% of supply. This provides robust protection against potential attacks, as an attacker would need to control a substantial portion of the staked supply to influence consensus.

SIMD-228 reflects a subtle but important evolution in this security model. Rather than maximizing staking participation, it aims to find an optimal balance between security and capital efficiency. The targeted staking range of 33-50% still provides strong security guarantees while freeing up capital for productive use.

This represents a more nuanced understanding of blockchain security economics—acknowledging that beyond certain thresholds, additional staking provides diminishing security returns while imposing significant opportunity costs on the ecosystem.

The Risks and Unknowns

Despite the potential benefits, SIMD-228 entails several significant risks that warrant careful consideration.

a) Market Volatility Feedback Loops

The proposed model creates a dynamic relationship between market conditions and inflation policy. During bull markets, high SOL prices may incentivize unstaking to capture profits, reducing staking participation and potentially triggering higher inflation—just when the market least needs additional supply.

Conversely, during bear markets, stakers might rush to secure whatever yield is available, increasing staking participation and decreasing inflation when additional staking rewards might help support the market.

The simulations included in the proposal documents suggest that these feedback loops could be manageable under most conditions. However, extreme market stress scenarios could create unexpected dynamics that destabilize the model.

b) Validator Concentration Risks

If SIMD-228 does lead to validator attrition as predicted, it could accelerate stake concentration among a smaller set of operators. This concentration creates both centralization risks (fewer entities controlling consensus) and systemic risks (correlated failures affecting a larger portion of the network).

The documents acknowledge this concern but frame it as an acceptable trade-off for improved capital efficiency. This perspective aligns with Solana's broader positioning as a performance-focused L1 that makes pragmatic decentralization compromises where necessary.

c) Implementation Timing Considerations

The transition period for SIMD-228 has been extended from 10 epochs to 50 epochs based on community feedback. However, some validators have argued that even this extended timeline may be insufficient to adapt their business models.

Additionally, the gap between SIMD-228 implementation and the promised vote cost reduction creates a potentially precarious period for marginal validators. If the vote cost reduction is delayed or less effective than anticipated, validator attrition could exceed projections.

What This Tells Us About Solana's Future

Beyond its immediate economic implications, SIMD-228 reveals much about Solana's strategic direction and vision for the future of L1 blockchains.

a) The Capital Efficiency Hypothesis

At its core, SIMD-228 represents a bold bet on capital efficiency as the primary driver of L1 success. This hypothesis posits that a blockchain's value comes not from security guarantees alone, but from enabling productive economic activity through efficient capital allocation.

As one contributor cited in the documents put it: "Solana is viewed as the home of internet capital markets (i.e., the next evolution of capitalism)." This framing positions Solana not merely as a technical infrastructure but as a new economic system with its own monetary policy.

b) From Security-First to Performance-First

Most first-generation proof-of-stake networks prioritized security above all else, often targeting extremely high staking participation (Cosmos, for instance, aimed for 67%). SIMD-228 signals a shift toward a more balanced approach that considers performance and capital efficiency as equally important design goals.

This evolution mirrors Solana's broader technical philosophy: making pragmatic trade-offs to optimize for real-world usage rather than theoretical ideals.

c) Market-Driven Governance

By implementing a market-responsive inflation model, Solana is effectively delegating aspects of monetary policy to market forces rather than relying on fixed parameters. This approach acknowledges the limitations of central planning and embraces the idea that markets can more efficiently discover optimal capital allocation.

As Max Kaplan, CTO of Sol Strategies, argued in support of SIMD-228: "It is better to be roughly right than precisely wrong." This pragmatic approach—prioritizing real-world experimentation over theoretical perfection—permeates Solana's governance philosophy.

Conclusion: A Monetary Policy Coming of Age

SIMD-228 represents Solana's monetary policy coming of age—evolving from a simplistic fixed inflation model to a dynamic system that responds to network conditions and prioritizes capital efficiency.

For retail investors, the immediate impact may be lower staking yields, but the long-term potential for a more vibrant, capital-efficient ecosystem could more than compensate. For validators, the path forward involves adaptation: either scaling up to compete in the MEV and priority fee markets or finding sustainable niches to serve specific community needs.

The greatest beneficiaries—venture capital firms and other large institutional holders—have remained relatively quiet in public debates, perhaps understanding that their interests are already well-served by the proposal. Meanwhile, DeFi protocols stand ready to absorb billions in newly liberated capital, potentially transforming Solana's financial ecosystem.

What's clear is that SIMD-228 is not merely a technical adjustment but a fundamental reimagining of how value flows through the Solana ecosystem. It reflects a maturing understanding of blockchain economics that moves beyond simplistic security models to embrace the complex reality of market-driven capital allocation.

Whether you support or oppose the changes, one thing is certain: after SIMD-228, Solana will never be the same. The network is choosing a path that prioritizes usage over hoarding, transaction activity over passive staking, and capital efficiency over maximal decentralization. This represents a distinctive vision for what a Layer 1 blockchain should be—one that will either prove prescient or cautionary in the years to come.

For those invested in Solana's ecosystem, now is the time to adapt to this new reality—because the greatest trick any investor can pull is seeing change coming before others do.

References

Solana Foundation. (2024). SIMD-228: Market-Based Emission Mechanism. Retrieved from https://github.com/solana-foundation/solana-improvement-documents/blob/main/proposals/0228-market-based-emissions.md

Resnick, M. (2024). I Support 228 Because I Want Solana to Win. Retrieved from https://x.com/MaxResnick1/status/1896316441869381914

Kankani, V., & Jain, T. (2024). Proposal for introducing a programmatic market-based emission mechanism based on staking participation rate. Solana Forum. Retrieved from https://forum.solana.com/t/proposal-for-introducing-a-programmatic-market-based-emission-mechanism-based-on-staking-participation-rate/3294

Mumtaz, M. (2024, March 4). [Twitter post]. Retrieved from https://twitter.com/0xMert_/status/1764753066818023809

Solana Compass. (2025). Solana Tokenomics. Retrieved from https://solanacompass.com/tokenomics

MostlyData. (2024). SIMD-228 Analysis Dashboard. FlipSide Crypto. Retrieved from https://flipsidecrypto.xyz/MostlyData_/simd-228-analysis-SJh-x5

Kaplan, M. (2025). In support of SIMD-228 [Twitter post]. Retrieved from https://x.com/maxekaplan/status/1896191334588846578

Marty, P. (2025) [Twitter Post]. Retrieved from https://x.com/martypartymusic/status/1898926716267216940?s=46&t=rjYucuZfSGfMliQL0yyTyg

Why optimum staking ratio is 67% for Cosmos and all Tendermint-based networks? https://www.reddit.com/r/cosmosnetwork/comments/rcgl6x/why_optimum_staking_ratio_is_67_for_cosmos_and/; Also see https://www.youtube.com/watch?v=uMo8MvpX0cM.

Acknowledgements:

First of all, I’d like to thank Lili Nuel for always supporting and pushing me to do better; She provided the first set of resources for this research document, for which I’m very grateful for. Thank you, Lili; Can’t wait to pay it forward;

I’d also like to thank Harri Obi; When I was overwhelmed with the resources before me; He was kind enough to share with me a particular resource that was instrumental in knowing what’s important to focus on and what to ignore or pay little attention to;

Subscribe to my newsletter

Read articles from Daniel Asaboro directly inside your inbox. Subscribe to the newsletter, and don't miss out.

Written by

Daniel Asaboro

Daniel Asaboro

Co-Lead, GDSC Unilag. Mobile Developer, Carus, Deliva Pro