The Impact of Open Banking on Payment Innovations and Consumer Experience

Jai Kiran Reddy Burugulla

Jai Kiran Reddy Burugulla

Introduction

Open Banking refers to the practice of providing third-party providers with access to consumer banking data, with the consumer’s consent, through secure Application Programming Interfaces (APIs). This model has gained significant traction in the financial industry due to its potential to foster innovation, improve payment systems, and enhance the overall consumer experience. By enabling greater interoperability between banks and fintech companies, Open Banking offers new opportunities for payment innovations and promises to reshape the way consumers engage with their financial services. This research explores how Open Banking is influencing payment innovations and transforming consumer experiences within the digital financial ecosystem.

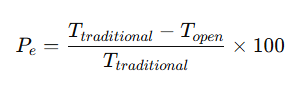

EQ: 1. Payment Efficiency Equation:

Open Banking: A Catalyst for Payment Innovation

Open Banking is fundamentally changing the landscape of payments by enabling more dynamic, efficient, and user-friendly payment solutions. Traditionally, payment systems were dominated by banks and payment processors that provided limited options and often required intermediaries, resulting in higher costs and slower processing times. Open Banking allows third-party providers to access consumer banking data securely and facilitate transactions directly, bypassing the need for traditional intermediaries.

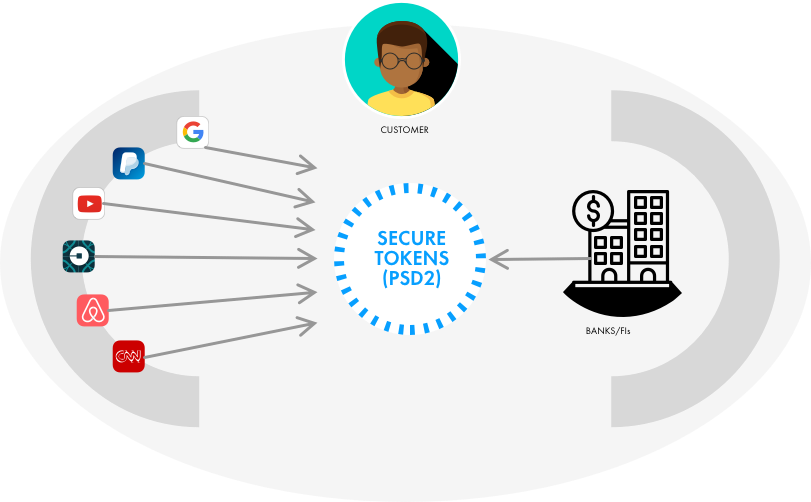

One of the most notable innovations resulting from Open Banking is the rise of Instant Payments. By linking accounts and facilitating direct transfers between consumers, businesses, and financial institutions, Open Banking accelerates the movement of funds in real time. The European Union’s PSD2 (Payment Services Directive 2) regulation, for example, has pushed financial institutions to provide customers with instant payment options. Instant payments have the potential to reduce transaction fees significantly, as well as the time it takes to transfer money between accounts. These faster transactions are especially crucial for industries such as e-commerce, where quick payment confirmation is essential for smooth customer experiences.

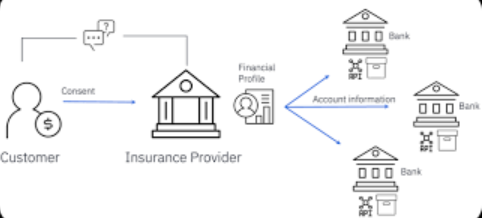

Another key innovation is Account Aggregation. Open Banking enables consumers to consolidate their financial information from various accounts (e.g., savings, checking, credit cards) into a single dashboard. Through this feature, users can track their financial health and manage payments more effectively. For example, services such as budgeting apps and financial management tools are leveraging Open Banking APIs to provide users with a comprehensive view of their finances. This increases transparency, offering a more holistic understanding of spending habits and making it easier for consumers to manage payments and improve their financial planning.

Furthermore, Payment Initiation Services (PIS) have emerged as a prominent innovation in the Open Banking ecosystem. PIS allows third-party providers to initiate payments directly from a consumer’s bank account, without the need for credit or debit cards. Services such as PayPal, Stripe, and Klarna have adapted these models to enable consumers to pay for goods and services seamlessly. With PIS, consumers can complete transactions more securely, bypassing the need to manually input card details and lowering the risk of fraud.

Enhancing Consumer Experience through Open Banking

Open Banking is designed to empower consumers by giving them greater control over their financial data and payment preferences. This has had a direct impact on enhancing the consumer experience, particularly in the realm of payment processes.

One of the most significant improvements has been personalized experiences. By having access to comprehensive banking data, third-party providers can offer highly tailored financial products and services that suit the individual needs of consumers. For example, lenders can offer loans with customized repayment terms based on a borrower’s financial history. Similarly, consumers can receive personalized payment options and advice, such as reminders for bill payments or suggestions for reducing credit card debt. These individualized offerings make consumers feel more in control and supported in managing their finances.

The integration of seamless payment solutions is another key benefit of Open Banking. Consumers no longer need to switch between different apps or payment platforms. Instead, Open Banking allows businesses to integrate payment functionalities directly into their websites or mobile apps, providing a frictionless experience. The ability to complete purchases or payments with just a few clicks, without having to input sensitive payment information every time, greatly enhances the convenience factor. The more intuitive and user-friendly the experience, the more likely consumers are to engage with the platform, resulting in higher user satisfaction.

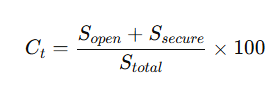

EQ:2. Consumer Trust Equation:

Moreover, Open Banking plays a critical role in security improvements in payment systems. One of the concerns consumers had with traditional banking was the vulnerability of their data, especially when making online payments. Open Banking addresses these concerns by enforcing strong authentication measures, such as two-factor authentication (2FA) and biometric verification. These security protocols ensure that only authorized individuals can access sensitive financial data, making payments more secure and instilling consumer trust in digital payment systems. As a result, consumers feel more comfortable adopting digital payment methods, leading to higher engagement with Open Banking-enabled platforms.

Additionally, cost-effectiveness is another factor improving the consumer experience. By eliminating intermediaries, Open Banking lowers the overall cost of payments. Traditional payment systems involve multiple parties, each adding fees to the transaction. Open Banking’s direct payment systems, on the other hand, allow consumers to bypass these fees, making payment solutions more affordable. This has the potential to democratize access to financial services, enabling even lower-income consumers to benefit from the advancements in payment technology.

Challenges and Future Outlook

Despite the many benefits of Open Banking, there are several challenges that need to be addressed for it to reach its full potential. One of the primary concerns is the standardization of APIs across different regions and institutions. For Open Banking to be effective, it requires a consistent approach to API development, ensuring interoperability across financial institutions and service providers. Without this, consumers may face compatibility issues when trying to connect different financial accounts or switch between service providers.

Another challenge is the adoption of Open Banking by consumers. Many people are still unfamiliar with Open Banking and may be hesitant to share their banking information with third-party providers, even though security measures are in place. Building trust and educating consumers on the benefits of Open Banking will be crucial in overcoming this barrier.

The future of Open Banking is promising, with increasing investment in fintech innovation and regulatory support. As more businesses and consumers embrace this model, we can expect further developments in payment technology that will continue to enhance consumer experiences and revolutionize the global payments landscape.

Conclusion

Open Banking has undeniably made a significant impact on payment innovations and consumer experience. By facilitating faster payments, offering personalized solutions, and improving security, Open Banking has transformed how consumers interact with their financial institutions. While challenges remain in terms of standardization and consumer adoption, the future of Open Banking is bright, with continued advancements set to further empower consumers and reshape the payments industry. As the ecosystem matures, we can expect even greater efficiency, convenience, and security, ultimately benefiting consumers and driving the next wave of financial innovation.

Subscribe to my newsletter

Read articles from Jai Kiran Reddy Burugulla directly inside your inbox. Subscribe to the newsletter, and don't miss out.

Written by