How RBI’s Third Consecutive Repo Rate Cut Can Impact India’s Bond & FD Market?

Vanya Gautam

Vanya GautamTable of contents

- What Is Repo Rate?

- What Happens When The Repo Rate Gets Cut?

- How RBI’s Repo Rate Cuts Impact Stock Market & Bond Market?

- Sensex Has Fallen On Both Repo Rate Cut Announcements This Year

- Sensex Reverses Its Trend To Rise After Third Repo Rate Cut

- How The Bond Market Reacted During April’s Repo Rate Cut Announcement

- India’s Bond Market Yields Had Begun To Fall Amid Rate Cut Expectations

- But, Not All Bonds Get Impacted Similarly

- Another Big Shift Being Seen In Bond Market

After two back-to-back repo rate cut announcements this year (in February and April), RBI has again cut the repo for the third consecutive time. After its MPC meeting’s conclusion today (6th June), the RBI announced a 50 bps repo rate cut, taking the total tally of repo rate cut to 100 bps (25 bps in February and April each this year and then 50 bps in June). The revised repo rate now stands at 5.50%, down from 6.00% after this recent rate cut.

This 50 bps repo rate has come at a time when there has been continued global uncertainty triggered by the US tariff moves and other geopolitical tensions and supply chain disruptions. Amidst all this, India’s central bank provided much needed relief by announcing this rate cut, and the RBI Governor Sanjay Malhotra also changed the policy stance to ‘Neutral’ from ‘Accommodative’.

Now, before we jump onto the expected impact of RBI’s third consecutive repo rate cut on your investments, especially the bond market, let us first catch the smaller fish here by understanding the concept of repo rate itself.

What Is Repo Rate?

Just like we borrow money from banks in the form of loans given at a particular lending rate such as 7% or 10%, banks borrow money from the RBI. And the rate at which the RBI lends to various commercial banks, is known as the repo rate. Simply put, it is the interest rate at which the RBI lends money to commercial banks, usually against government securities put as collateral.

What Happens When The Repo Rate Gets Cut?

Impact On Loans

When the RBI cuts the repo rate, banks can borrow money from the RBI at a lower interest rate. This way, the banks also tend to pass on this benefit of lower interest rates to borrowers like you and me by lowering the loan interest rates. With lower interest rates on offer, people get to avail loans at cheaper rates, as well as their existing loans which are floating rates, get cheaper too.

So basically, repo rate cuts act like a boost button for the economy, with cheaper loans and more liquidity. These three back-to-back repo rate cuts by the RBI this year are expected to continue the trend of falling loan interest rates in banks, which is good for both new and existing borrowers of loans such as home loan, car loan, personal loan, etc.

Impact On Fixed Deposits

RBI’s repo rate cuts not only leads to a drop in bank’s lending rates, but also the FD (Fixed Deposit) rates. Even before this third consecutive repo rate cut, the previous two back-to-back repo rate cuts had already resulted in FD rates of all banks to fall, with an SBI research report indicating that FD rates had already reduced in the range of 30-70 bps since February 2025’s repo rate cut.

And now, this third consecutive repo rate cut by the RBI is expected to make the FD rates fall further. Moreover, the SBI research report had even mentioned that repo rate is further expected to fall upto 100 bps more in this financial year of 2025-26, signaling that FD rates too are expected to continue to fall in this FY26.

Impact On Bonds

A repo rate cut typically affects the bond market to a great extent because interest rate changes have a direct impact on bond prices and yields since the two move in opposite directions. When interest rates fall due to repo rate cut, bond prices go up.

For the unversed, bond yields are the returns an investor can expect to earn until maturity. So, when bond yield falls, the price of the bond goes up. This is because the interest paid by the bond (the coupon) stays the same, but as new bonds in the market start offering lower returns, your bond with a higher fixed interest becomes more valuable. So, more people want to buy it, which pushes its price up.

How RBI’s Repo Rate Cuts Impact Stock Market & Bond Market?

Repo rate cuts impact both the stock market as well as the bond market in their own separate ways. Given that the RBI has already cut the repo rate not once but twice this year, let us look back at how the markets reacted in February and April, which can give us a signal of what to expect in case of a repo rate cut this time:

Sensex Has Fallen On Both Repo Rate Cut Announcements This Year

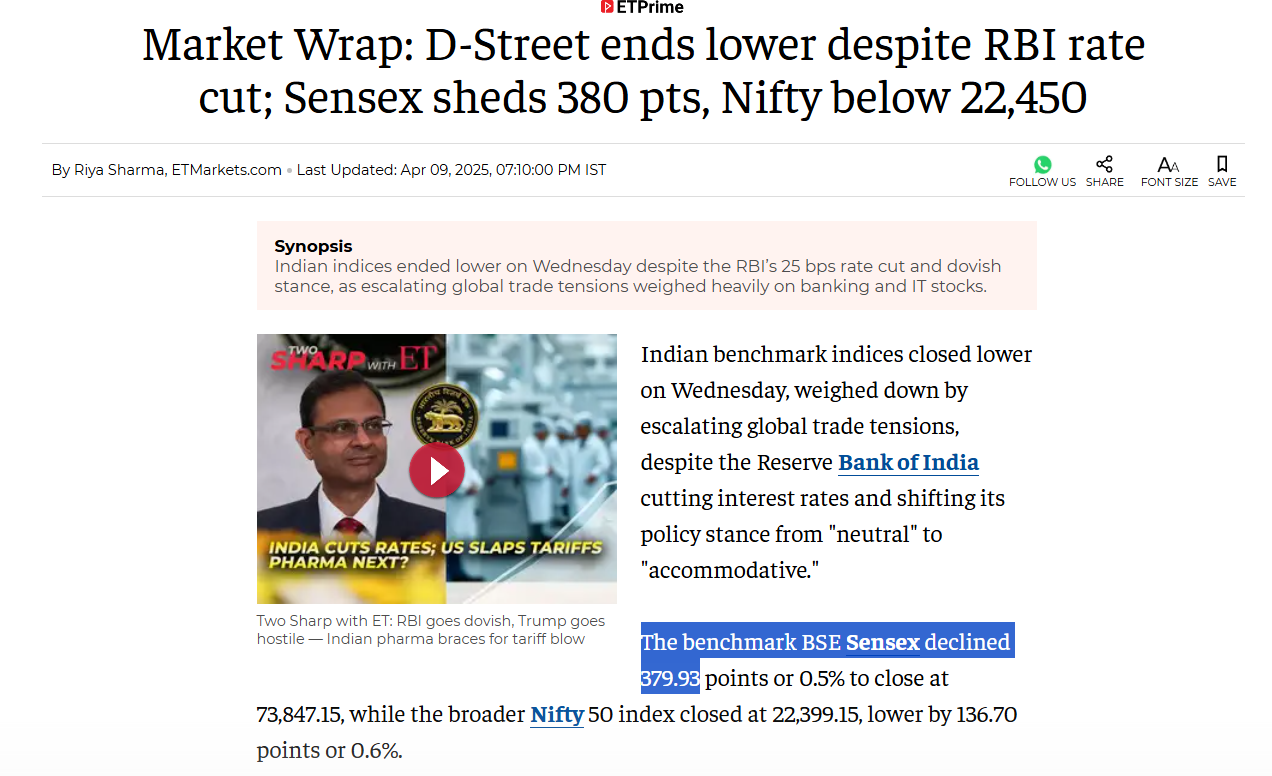

MPC Meeting Of April 2025: Despite the RBI providing a relief to borrowers with a widely anticipated repo rate cut, the Sensex had fallen nearly 400 points after the MPC announcement on April 9th. There were two key reasons behind the slump in the stock market despite a repo rate cut.

Firstly, the RBI’s decision to shift its policy stance from ‘accommodative’ to ‘neutral’ was believed to have caught the investors off guard, given that it signaled a more measured approach going forward. Secondly, the stock market had remained volatile throughout that day amid the US President Donald Trump's announcement of a 104% tariff on Chinese goods.

MPC Meeting Of February 2025: Even if we look at the repo rate cut of February 2025, which was the first one this year, the Sensex had still fallen despite the RBI’s rate cut relief. Sensex had ended the day of 7th February with a drop of around 200 points as the first repo rate cut of 2025 failed to cheer the investors, primarily because experts mentioned that investors were disappointed by the absence of any major liquidity measures for the economy, despite an anticipation regarding the same. Market sentiment was also adversely impacted by a slight downward revision in the RBI's near-term growth forecast, which was influenced by global trade policies and inflation concerns.

Sensex Reverses Its Trend To Rise After Third Repo Rate Cut

Reversing its previous trend of falling after both repo rate cuts this year, the Sensex rose 746.95 points to end the day (6th June) at 82,188. RBI’s surprise repo rate cut of 50 bps instead of 25 bps is being seen as one of the key reasons behind the market surge.

How The Bond Market Reacted During April’s Repo Rate Cut Announcement

The last time when the RBI did the repo rate cut announcement in April 2025, bond yields dropped after the announcement. India's benchmark 10-year bond yield dropped to a marginally lower level of 6.50% against earlier one of 6.51%, after the second consecutive repo rate cut in April this year. Even a few days before that repo rate cut, India’s benchmark 10-year bond yields had fallen sharply from 6.58 per cent to 6.49 per cent year-on-year, after the RBI’s announcement that it would buy Rs 80,000 crore worth of bonds in April.

And, what we are seeing this time is no different, with the falling bond yields signaling a repo rate cut expectation.

India’s Bond Market Yields Had Begun To Fall Amid Rate Cut Expectations

Ahead of the third expected repo rate cut by the RBI this year which eventually did happen, the government bond yields had already begun to decline in the last few days, as bond traders started adding positions especially in the 10-year part of the yield curve, ahead of the RBI's monetary policy decision on 6th June.

Less than a week ago, India's 10-year benchmark 6.33% 2035 bond yield pared its earlier losses to end flat at 6.2308% on Friday. As per a Reuters report, bond traders are anticipating the yield to move between 6.18% and 6.26%.

If we check the recent movement in the bond market this week, the yield on the new benchmark 10-year bond ended at 6.2022% on Tuesday, which is a drop in comparison to the previous day’s close of 6.2144%. Even the relatively liquid five-year bond yields ended at 5.8520%, thus further steepening the yield curve ahead of the expectation of RBI’s repo rate cut decision.

So clearly, the bond market was also expecting a rate cut from the RBI, which is why there has been bullish positioning in the days leading up to the MPC meeting decision.

But, Not All Bonds Get Impacted Similarly

While the above mentioned instances show how that the yields and prices of the highest (AAA) rated bonds get significantly impacted from RBI’s repo rate cuts, the case is different for relatively lower rated bonds, such as A rated bonds.

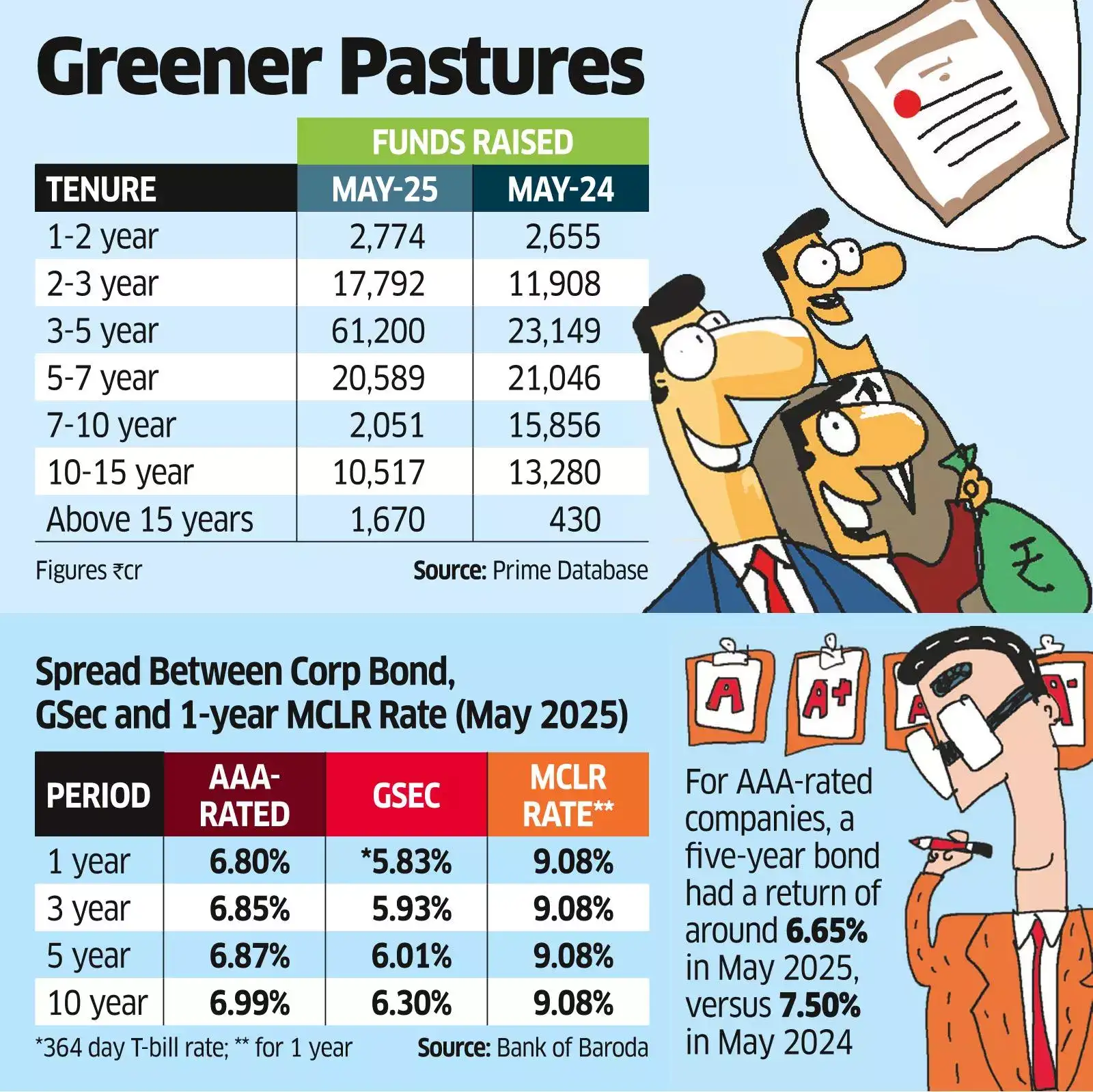

Here’s a detailed chart that shows the movement of yield rates across repo rate, FD and A-rated bonds.

Sources: RBI Statistics Data – Structure of Interest Rates, PRIME Database, BankBazaar

As we can see from the above graph, yields of A-rated bonds are less sensitive to repo rate movements than FDs, implying that the performance of A rated bonds actually doesn’t change much especially when compared to AAA ones. This goes on to provide a better arbitrage opportunity and more consistent returns for A-rated bonds.

Now let us make you understand one of the key reasons behind the relatively lower impact on bonds. Given that banks can borrow money from the RBI for their operations, it gets cheaper for banks to borrow when the RBI announces a repo rate cut, thus they are able to reduce the rates they pay customers for fixed deposits. However, corporates and NBFCs however cannot borrow from the RBI and hence a reduction in the repo rate does not directly reduce their cost of borrowing. While bond yields also tend to go lower after repo rate cut, the change will not be as significant or quick as in the case of bank FDs.

Another Big Shift Being Seen In Bond Market

Some recent media reports have shown a new trend in India’s bond market. With banks being slow in passing on the benefit of previous rate cuts and falling bond yields looking tempting, the top rated-corporate companies are increasingly turning to India’s bond market, with a higher preference for short-term bonds. Corporates have reportedly issued Rs 61,200 crore in up to five-year bonds in May 2025, which is a nearly three times jump from the funds raised a year ago (in May 2024) for the same tenure.

Source: ET

All this has happened after the RBI’s nearly $100-billion infusion of liquidity into the banking system since December 2024, which has led to a sharper fall in short-term bond yields in comparison to their long-term peers. It’s fair to say that this has been triggering a change in the way companies borrow, which is visible from this trend, right?

Subscribe to my newsletter

Read articles from Vanya Gautam directly inside your inbox. Subscribe to the newsletter, and don't miss out.

Written by

Vanya Gautam

Vanya Gautam

I am a millennial centric (and maybe now Gen Z too) content creator who aims to simplify the world of personal finance, so that your hard earned money doesn’t end up hardly working for you. After working in this field for over 7 years, my priority remains the same-to make personal finance less boring and more jargon free through my unbiased and well-researched content!